May 13, 2026

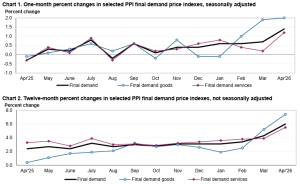

According to the U.S. Bureau of Labor Statistics, the Producer Price Index (PPI) for final demand increased 1.4% in April, seasonally adjusted. This follows a 0.7% rise in March and a 0.6% increase in February. The April advance marks the largest monthly gain since March 2022. On an unadjusted basis, the index for final demand rose 6.0% over the 12 months ended April, the largest 12-month increase since December 2022.

Nearly 60% of April’s overall gain was driven by a 1.2% increase in final demand services, while final demand goods prices rose 2.0%.

Excluding foods, energy, and trade services, the PPI for final demand increased 0.6%, matching the pace last seen in October 2025. Over the past year, this index has advanced 4.4%, the largest 12-month rise since February 2023.

Final demand goods

Prices for final demand goods increased 2.0%, following a 1.9% rise in March. More than three-quarters of the gain came from a 7.8% jump in energy prices. Goods excluding food and energy rose 0.7%, and food prices increased 0.2%.

A notable driver was a 15.6% surge in gasoline prices, accounting for more than 40% of the overall goods increase. Other contributors included higher prices for jet fuel, diesel fuel, fresh and dry vegetables, industrial chemicals, and residual fuels. Offsetting movements included a 49.7% decline in chicken eggs, along with lower prices for nonferrous scrap and residential natural gas.

Final demand services

The index for final demand services rose 1.2%, the largest increase since March 2022. About two-thirds of the gain came from a 2.7% jump in trade services margins. Transportation and warehousing services rose 5.0%, and services excluding trade, transportation, and warehousing edged up 0.1%.

A 3.5% increase in margins for machinery and equipment wholesaling was a major factor in the overall advance. Additional contributors included gains in truck transportation of freight; fuels and lubricants retailing; health, beauty, and optical goods retailing; chemicals and allied products wholesaling; and legal services. Declines were recorded in portfolio management, food retailing margins, and margins for metals, minerals, and ores wholesaling.

Disclaimer:

Analyst Certification – The views expressed in this research report accurately reflect the personal views of Mayberry Investments Limited Research Department about those issuer (s) or securities as at the date of this report. Each research analyst (s) also certify that no part of their compensation was, is, or will be, directly or indirectly, related to the specific recommendation(s) or view (s) expressed by that research analyst in this research report.

Company Disclosure – The information contained herein has been obtained from sources believed to be reliable, however its accuracy and completeness cannot be guaranteed. You are hereby notified that any disclosure, copying, distribution or taking any action in reliance on the contents of this information is strictly prohibited and may be unlawful. Mayberry may effect transactions or have positions in securities mentioned herein. In addition, employees of Mayberry may have positions and effect transactions in the securities mentioned herein.