May 21, 2026

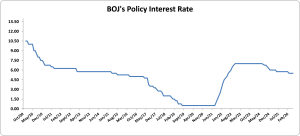

The Bank of Jamaica’s Monetary Policy Committee unanimously held the policy rate at 5.50 per cent following its 19–20 May meeting, citing the escalating Middle East conflict and its upward pressure on international commodity prices, particularly crude oil. Alongside the rate hold, BOJ extended its special FX interventions — including direct supply to energy-sector entities and pre-announced market sales — and confirmed a US$30 million B-FXITT standard sale on 21 May.

The Committee acknowledged that the 4.0 to 6.0 per cent inflation target band is unlikely to hold over the next two quarters. Headline inflation was 4.3 per cent at April 2026 (unchanged from March but above BOJ’s projection) and core inflation ticked up to 4.1 per cent. Inflation is now expected to breach the target over the June and September 2026 quarters before gradually moderating as oil supplies normalise — though post-Hurricane Melissa reconstruction spending could partly offset that decline. The imported-inflation channel is already active: WTI crude rose 21.5 per cent in the March quarter, grains 5.2 per cent, and shipping 13.0 per cent, while US inflation has reaccelerated to 3.3 per cent.

Business inflation expectations 12 months ahead jumped to 7.1 per cent from 6.5 per cent, alongside higher expected JMD depreciation — though deposit dollarisation has stayed stable, which explains BOJ’s posture of holding the rate, leaning on FX interventions, and waiting to see if expectations harden. Real GDP growth for FY2026/27 is projected at 1.0 to 3.0 per cent with downside risks centred on tourism, while strong foreign reserves are expected to cushion the external accounts. The Fed’s hold at 3.50–3.75 per cent removes any external pressure on BOJ to move, and private sector credit growth has slowed to 6.5 per cent from 7.8 per cent the prior quarter.

The guidance tilts hawkish: risks to inflation are skewed to the upside, driven by a potential broadening of the Middle East conflict, El Niño effects, rising expectations, and post-hurricane fiscal spending. The MPC was explicit that it stands ready to tighten if the conflict is protracted and price pressures become sustained. For now, the 5.50 per cent floor is being defended through FX intervention rather than hikes, with the next decision scheduled for 29 June 2026 — by which point April–May inflation prints and the oil trajectory should clarify the path forward.

Disclaimer:

Analyst Certification – The views expressed in this research report accurately reflect the personal views of Mayberry Investments Limited Research Department about those issuer(s) or securities as at the date of this report. Each research analyst (s) also certify that no part of their compensation was, is, or will be, directly or indirectly, related to the specific recommendation(s) or view(s) expressed by that research analyst in this research report.

Company Disclosure – The information contained herein has been obtained from sources believed to be reliable, however its accuracy and completeness cannot be guaranteed. You are hereby notified that any disclosure, copying, distribution or taking any action in reliance on the contents of this information is strictly prohibited and may be unlawful. Mayberry may effect transactions or have positions in securities mentioned herein. In addition, employees of Mayberry may have positions and effect transactions in the securities mentioned herein.