April 2, 2026

IronRock Insurance Company Limited (ROC)

Audited financials for the twelve months ended December 31, 2025:

IronRock Insurance Company Limited (ROC) for the twelve months ended December 31, 2025, reported a 22% increase in Insurance Revenue totalling $2.14 billion compared to $1.75 billion in the corresponding period last year. The growth was broad-based across all lines of business, with the Liability segment leading expansion at 83% year-over-year, followed by Other (+32%), Motor (+14%), and Property (+17%).

Insurance Service Expenses increased significantly by 64% to $1.11 billion (2024: $678.02 million), driven primarily by a surge in incurred claims and directly attributable costs to $751.55 million (2024: $396.31 million) stemming from the impact of Hurricane Melissa. The company recognised approximately $1.5 billion in additional insurance contract liabilities related to hurricane-related claims across the property and related portfolios, representing management’s best estimate of ultimate costs. Net Expenses from Reinsurance Contracts Held remained largely stable at $931.14 million (2024: $926.18 million), as robust reinsurance recoveries largely offset elevated ceded premiums.

Consequently, the Insurance Service Result decreased by 36% to $96.18 million (2024: $150.61 million). Net Investment Income declined marginally by 2% to $102.65 million relative to $104.30 million in the prior year, as interest revenue of $81.19 million (2024: $79.70 million) was partially offset by a contraction in other investment revenue to $22.85 million (2024: $29.57 million).

Other income for the twelve months ended December 31, 2025 amounted to $3.58 million, a 62% decline relative to the $9.52 million reported in 2024. Other operating expenses totalled $198.97 million, a 14% increase from the corresponding period (2024: $174.79 million). A new finance charge of $17.29 million was recorded in the period, reflecting interest on lease liabilities arising from the company’s relocation to its new head office at 33½ Hope Road, Kingston 10 under IFRS 16.

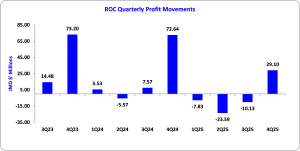

Loss before taxation for the twelve months ended December 31, 2025 amounted to $9.51 million (2024: profit of $93.28 million). A tax charge of $2.95 million was incurred (2024: tax charge of $12.57 million). As a result, the Net Loss for the twelve-month period was $12.45 million, a reversal from the net profit of $80.71 million reported in 2024. Tax losses available for carry-forward as at December 31, 2025 amounted to approximately $22.68 million.

Consequently, Loss Per Share for the twelve months amounted to $0.06 (2024: EPS of $0.38). The number of shares used in this calculation was 214,000,000. Notably, ROC’s stock price closed at $2.65 on April 1, 2026, implying a Price-to-Book ratio of 0.73 times, with the stock trading below book value.

A dividend of $0.09 per stock unit was declared for the period (2024: $0.10), representing total dividends paid of $19.26 million.

Balance Sheet Highlights

The company’s total assets expanded significantly to $4.58 billion (2024: $1.69 billion), a 171% increase year-over-year. This movement was driven primarily by a 383% surge in Reinsurance Contract Assets to $2.12 billion (2024: $438.64 million), as well as a 449% increase in Cash and Cash Equivalents to $1.30 billion (2024: $237.65 million).

Insurance Contract Liabilities correspondingly expanded to $3.53 billion (2024: $810.77 million). The company also recognised a Right-of-Use Asset of $195.96 million and corresponding Lease Liabilities of $206.23 million following the execution of a five-year lease for its new head office premises.

Stockholders’ equity closed at $781.78 million (2024: $811.48 million), representing a book value per share of $3.65 (2024: $3.79). The decline reflects the net loss and dividends paid during the period, partially offset by other comprehensive income of $2.02 million from fair value movements on FVOCI financial assets.

The company’s Minimum Capital Test (MCT) ratio stood at 166% as at December 31, 2025 (2024: 302%), remaining above the Financial Services Commission’s mandated minimum of 150%, notwithstanding the material impact of Hurricane Melissa on the capital position.

Disclaimer:

Analyst Certification -The views expressed in this research report accurately reflect the personal views of Mayberry Investments Limited Research Department about those issuer (s) or securities as at the date of this report. Each research analyst (s) also certify that no part of their compensation was, is, or will be, directly or indirectly, related to the specific recommendation(s) or view (s) expressed by that research analyst in this research report.

Company Disclosure -The information contained herein has been obtained from sources believed to be reliable, however its accuracy and completeness cannot be guaranteed. You are hereby notified that any disclosure, copying, distribution or taking any action in reliance on the contents of this information is strictly prohibited and may be unlawful. Mayberry may affect transactions or have positions in securities mentioned herein. In addition, employees of Mayberry may have positions and effect transactions in the securities mentioned herein.